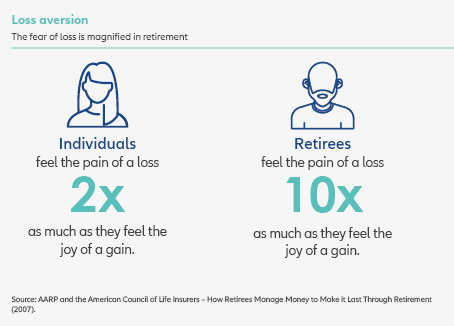

Recently, market volatility has been in the headlines and, for the 710,000 people who intend to retire within the next five years and the 4.2 million Australians1 already retired, protecting one’s super or pension from extreme market fluctuations is a key priority.

We only need to look back to 2008 to understand why a defensive mindset is prevalent in older Australians. The impact of the GFC still haunts those who retired with drastically depleted super balances, and to this day serves as a cautionary tale for many who are approaching retirement.

With the multitude of unknowns that exist in retirement, it’s common to see a client’s risk profile shift to a more conservative attitude of minimising risk and creating greater certainty of income.

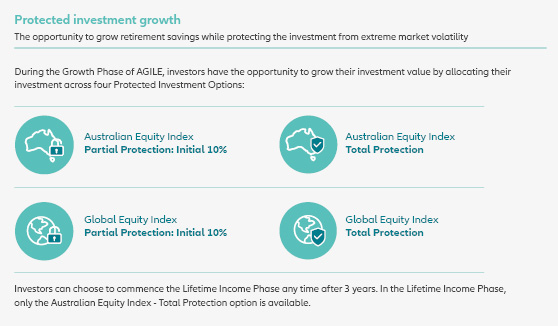

Growth vs protection: the trade-off

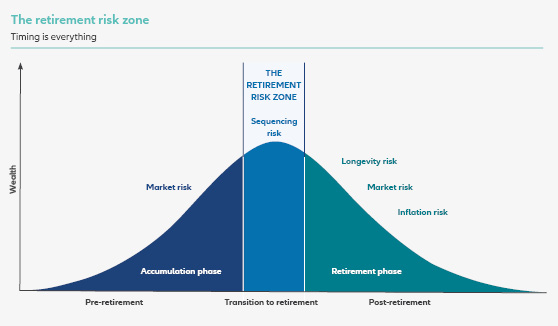

Like so many things in life, retirement is all about timing. In a perfect world, we’d all retire when markets are experiencing very little volatility. However, many people don’t have the luxury of choosing when to retire – in fact, almost 1 in 5 older Australians1 are forced to stop working before they are ready to do so (usually due to job loss or redundancy, ill-health or to care for family members).

Research has shown that market conditions just before and at the time of retirement can have a significant impact on how long savings last – and can be the difference between living comfortably or living frugally in retirement.

A ‘retirement risk zone’ occurs around 7 years before retirement, when savings are at their highest level but are most vulnerable to market volatility.

.jpeg)